Introduction: The Essence of Financial Channels

Hello, everyone! Welcome to this insightful article on financial intermediation and direct financing. In the realm of finance, these two mechanisms are pivotal in facilitating the flow of funds. Let’s embark on this journey of understanding their distinctions and significance.

Financial Intermediation: The Bridge Between Savers and Borrowers

Financial intermediation essentially involves the presence of intermediaries, such as banks and non-banking financial institutions. These entities act as the middlemen, connecting those with surplus funds (savers) to those in need of funds (borrowers). The process typically entails savers depositing their funds with the intermediaries, who, in turn, lend these funds to borrowers. This mechanism offers several advantages, including risk diversification, liquidity provision, and expertise in credit assessment.

Direct Financing: A Direct Link Between Savers and Borrowers

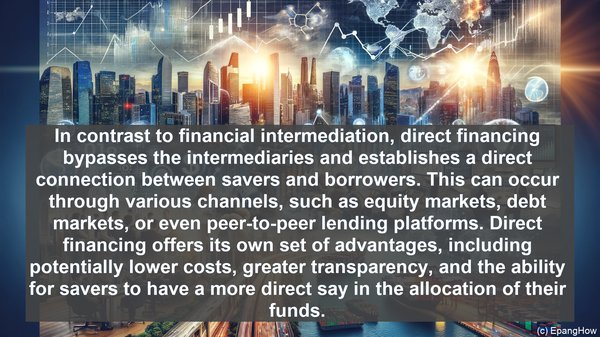

In contrast to financial intermediation, direct financing bypasses the intermediaries and establishes a direct connection between savers and borrowers. This can occur through various channels, such as equity markets, debt markets, or even peer-to-peer lending platforms. Direct financing offers its own set of advantages, including potentially lower costs, greater transparency, and the ability for savers to have a more direct say in the allocation of their funds.

The Pros and Cons of Financial Intermediation

Financial intermediation has long been a dominant mechanism, primarily due to its ability to address certain inherent challenges. For instance, intermediaries can pool funds from multiple savers, thereby enabling larger-scale lending. Additionally, their expertise in credit assessment helps mitigate the risk associated with lending. However, financial intermediation is not without its drawbacks. The presence of intermediaries adds an additional layer of costs, which can be passed on to borrowers. Moreover, the intermediaries’ own risk appetite and regulatory constraints can impact the availability and terms of funds.

The Advantages and Limitations of Direct Financing

Direct financing, on the other hand, offers a more streamlined approach. By eliminating intermediaries, it can potentially reduce costs, making it an attractive option for certain borrowers. Furthermore, direct financing mechanisms, such as equity markets, can provide a platform for businesses to raise capital for growth and expansion. However, direct financing is not without its challenges. For instance, the absence of intermediaries means that the onus of credit assessment and risk management falls directly on the savers. This can be a significant burden, especially for individual investors with limited expertise.

Real-World Applications: When Each Mechanism Shines

In the real world, the choice between financial intermediation and direct financing depends on various factors. For instance, in situations where there is a need for specialized expertise in credit assessment, financial intermediation can be the preferred route. On the other hand, for businesses looking to raise capital quickly and efficiently, direct financing mechanisms, such as initial public offerings (IPOs) or bond issuances, can be more suitable. It’s important to note that in many cases, a combination of both mechanisms is employed, striking a balance between efficiency and risk management.